NCERT Solutions for Class 11 Economics Chapter 6 - Non Competitive Markets

NCERT Solutions for Class 11 Economics Chapter 6 Free PDF Download

Please Click on Free PDF Download link to Download the NCERT Solutions for Class 11 Economics Chapter 6 Non Competitive Markets

26. What would be the shape of the demand curve so that the total revenue curve is

(a) a positiv ely sloped straight line passing through the origin?

(b) a horizontal line?

Ans. (a) The slope of the demand curve will be a horizontal line parallel to x-axis when revenue curve is a positively sloped line.

(b) Demand curve will be downward sloping when total revenue is a horizontal line.

| Quantity | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

| Marginal Revenue | 10 | 6 | 2 | 2 | 2 | 0 | 0 | 0 | -5 |

27. From the schedule provided below calculate the total revenue, demand curve and the price elasticity of demand:

Ans.

| Quantity (Q) | Marginal Revenue (MR) | Total Revenue (TR) | Demand Curve AR = TR/Q | Price Elasticity of Demand E d=(ΔQ/ΔP)×P/Q |

| 1 | 10 | 10 | 10/1=10 | - |

| 2 | 6 | 10 + 6 = 16 | 16/2=8 | (1/2)×(10/1)=5 |

| 3 | 2 | 16 + 2 = 18 | 18/3=6 | (1/2)×(8/2)=52 |

| 4 | 2 | 18 + 2 = 20 | 20/4=5 | (1/1)×(6/3)=2 |

| 5 | 2 | 20 + 2 = 22 | 22/5=4.5 | (1/0.5)×(5/4)=2.5 |

| 6 | 0 | 22 + 0 = 22 | 22/6=3.6 | (1/0.9)×(4.5/5)=1 |

| 7 | 0 | 22 + 0 = 22 | 22/7=3.1 | (1/0.5)×(3.6/6)=1.2 |

| 8 | 0 | 22 + 0 = 22 | 22/8=2.7 | (1/0.4)×(3.1/7)=1.1 |

| 9 | -5 | 22 - 5 = 17 | 17/9=1.9 | (1/0.8)×(2.7/9)=0.38 |

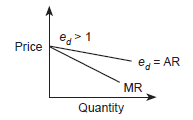

28. What is the value of the MR when the demand curve is elastic?

Ans. The relationship betwen MR and elasticity of demand can be depicted as follows :

$$MR=p(1-\frac{1}{e_d})\\\text{When demand curve is elastic }(e_d > 1), the\\\text{value of}\frac{1}{e_d}\text{will always be < 1.}\\\text{Hence, MR will always be positive (MR > 1).}$$

29. A monopoly firm has a total fixed cost of ₹100 and has the following demand schedule:

| Quantity | Price |

| 1 | 100 |

| 2 | 90 |

| 3 | 80 |

| 4 | 70 |

| 5 | 60 |

| 6 | 50 |

| 7 | 40 |

| 8 | 30 |

| 9 | 20 |

| 10 | 10 |

Find the short run equilibrium quantity, price and total profit. What would be the equilibrium in the long run? In case the total cost was ₹1000, describe the equilibrium in the short run and in the long run.

Ans. Total fixed cost (TFC) = ₹100

Let the Total Variable Cost (TVC) = ₹0

Total Cost (TC) = TFC + TVC

= 100 + 0

TC = ₹100

| Quantity (Q) | Price (P) | TR (P×Q) | TFC | TC | Total Profit (TR – TC) |

| 1 | 100 | 100 | 100 | 0 | 100 |

| 2 | 90 | 180 | 100 | 100 | 80 |

| 3 | 80 | 240 | 100 | 140 | 100 |

| 4 | 70 | 280 | 100 | 180 | 100 |

| 5 | 60 | 300 | 100 | 200 | 100 |

| 6 | 50 | 300 | 100 | 200 | 100 |

| 7 | 40 | 280 | 100 | 180 | 100 |

| 8 | 30 | 240 | 100 | 140 | 100 |

| 9 | 20 | 180 | 100 | 80 | 100 |

| 10 | 10 | 100 | 100 | 0 | 100 |

Profit will be maximum at 6th unit, where

TR – TC is ₹200.

Short run equilibrium price is ₹50 and

Profit = TR – TC

= 300 – 100 = 200

and equilibrium quantity will be 6 units.

In Long Run,

Profit = TR – TC

= 300 – 1000 = – 700

The firm is incurring loss in the long run and is in profit in the short run.

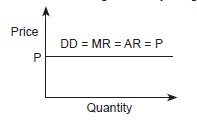

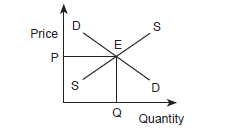

30. If the monopolist firm of Question 3, was a public sector firm. The government set a rule for its manager to accept the government fixed price as given (i.e., to be a price taker and therefore behave as a firm in a perfectly competitive market), and the government decides to set the price so that demand and supply in the market are equal. What would be the equilibrium price, quantity and profit in this case?

Ans. When a monopolist firm accepts the prices fixed by the government, it will behave like a perfectly competitive firm. Therefore, the prices set by the government will make the demand and supply equal.

Hence, the fim will earn normal profits

Equilibrium Price = P

Equilibrium Quantity = Q

Profit = Normal Profit

31. Comment on the shape of the MR curve in case the TR curve is a

(i) positively sloped straight line,

(ii) horizontal straight line.

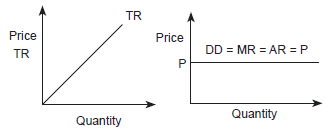

Ans. (i) If the TR curve is positively sloped straight line then, the MR curve will be a horizontal line. It is the condition of perfect competition, where the MR and the demand curve will be same with the AR constant at different outputs.

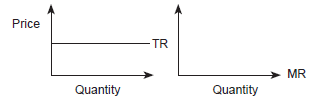

(ii) If TR curve is a horizontal straight line, then MR will be zero.

This is because of the fact that if TR is zero, there will no incremental or additional revenue at any level of output, thereby making MR = 0.

32. The market demand curve for a commodity and the total cost for a monopoly firm producing the commodity is given by the schedules below. Use the information to calculate the following:

| Quantity | Price |

| 0 | 52 |

| 1 | 44 |

| 2 | 37 |

| 3 | 31 |

| 4 | 26 |

| 5 | 22 |

| 6 | 19 |

| 7 | 16 |

| 8 | 13 |

| Quantity | Total Cost |

| 0 | 10 |

| 1 | 60 |

| 2 | 90 |

| 3 | 100 |

| 4 | 102 |

| 5 | 105 |

| 6 | 109 |

| 7 | 115 |

| 8 | 125 |

(a) The MR and MC schedules.

(b) The quantites for which the MR and MC are equal.

(c) The equilibrium quantity of output and the equilibrium price of the commodity.

(d) The total revenue, total cost and total profit in equilibrium.

Ans. (a)

(b) At 6th unit MR and MC are equal i.e., 4.

(c) Equilibrium is when MR = MC, therefore, 6th unit is the equilibrium quantity and 19 will be the equilibrium price.

(d) At equilibrium 6th unit of output.

TR = 114

TC = 109

Profit = TR – TC

= 114 – 109 = ₹5.

33. Will the monopolist firm continue to produce in the short run if a loss is incurred at the best short run level of output?

Ans. A monopolist firm can earn losses in the short run if price < minimum AC.

If price falls below the miniumm AVC, the firm will stop the production, as the firm becomes incompetent to bear its cost.

If the price is between the minimum AVC and minimum AC, the firm will continue to produce.

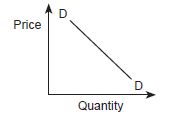

34. Explain why the demand curve facing a firm under monopolistic competition is negatively sloped.

Ans. A firm in monopolistic competition sells products that are differentiated from its competitor's product. Therefore, the monopolistic firm will lower the cost to increase the demand. Because the differentiated products are substitutes to each other, the demand for the commodities tends to be elastic. Because of this reason, the demand curve for a firm under monopolistic competition is negatively sloped.

| Quantity (Q) | Price (P) | Total Revenue = Q × P | MR (TRn – TRn – 1) | Total Cost | MC (TCn – TCn – 1) |

| 0 | 52 | 0 | 0 | 10 | — |

| 1 | 44 | 44 | 44 | 60 | 50 |

| 2 | 37 | 74 | 30 | 90 | 40 |

| 3 | 31 | 93 | 19 | 100 | 10 |

| 4 | 26 | 104 | 11 | 102 | 2 |

| 5 | 22 | 110 | 6 | 105 | 3 |

| 6 | 19 | 114 | 4 | 109 | 4 |

| 7 | 16 | 112 | −2 | 115 | 6 |

| 8 | 13 | 104 | −8 | 125 | 10 |

35. What is the reason for the long run equilibrium of a firm in monopolistic competition to be associated with zero profit?

Ans. In monopolistic competition, firm's products are unique and have partial competition. Also because of the free entry and exit of firms, the long run equilibrium price will be the same and the firm will earn zero economic profit or normal profit.

36. List the three different ways in which oligopoly firms may behave.

Ans.

- Each firm is relatively large when compared to the size of the market. As a result, each firm is in a position to affect the total supply in the market, and thus influences the market price. Therefore, the level of output in the industry, the level of prices, as well as the profits are decided on the behaviour of the firm.

- The firms can decide to form a ‘cartel’ which will act as a monopoly. A cartel is a group of sellers to become one single seller.

- The firms can decide to compete with each other. So, the market price keeps falling as long as firms keep cutting each other’s prices. This situation will lead to perfectly competitive market.

37. If duopoly behaviour is one that is described by Cournot, the market demand curve is given by the equation q = 200 – 4p, and both the firms have zero costs, find the quantity supplied by each firm in equilibrium and the equilibrium market price.

Ans. q = 200 – 4p

In this situation, the demand curve being a straight line and firms having 0 costs, a duopolsitic firms will find the best to supply goods amounting to half of the maximum demand in order to gain maximum profit.

at p = 0

Market demand is

q = 200 – 4p

= 200 – 4(0)

= 200

If firm B is not involved in any production. Then market demand for A = 200 units.

supply =200/2=100 units

(half of maximum market demand)

Firm B will now have market demand

= 200 – 100 = 100 units

supply=100/2=50 units

If firm B produced 50 units, A need to have a demand

= 200 – 50

= 150 units

A will produce = 150/2 = 75 units in order to earn profits.

| Round | Firms | Quantity supplied |

| 1 | B | 0 |

| 2 | B | $$\frac{1}{2}×200=100$$ |

| 3 | B | $$\frac{1}{2}(200-\frac{1}{2}×200)=\frac{1}{2}-\frac{200}{4}$$ |

| 4 | A | $$\frac{1}{2}[200-\frac{1}{2}(200-\frac{1}{2}×200)]=\frac{200}{2}-\frac{200}{4}+\frac{200}{8}$$ |

| 5 | B | $$\frac{1}{2}[200-\frac{1}{2}[200-\frac{1}{2}(200-\frac{1}{2}×200)]]=\frac{200}{2}-\frac{200}{4}+\frac{200}{8}-\frac{200}{16}$$ |

At equilibrium, both the firms A and B will have an output of 200/3 units.

Market supply =(200/3)+(200/3)=(400/3)

Equilibrium output = 400/3

Pricing this in equations:

q = 200 – 4p

4p = 200 – q

p=50-(q/4)

p=50-(1/4)×(400/3)

=50-(100/3)=50/3

Therefore, equilibrium price =50/3

38. What is meant by prices being rigid? How can oligopoly behaviour lead to such an outcome?

Ans. Prices being rigid means a situation where price does not change when demand changes. It may happen that a firm changes its price by more units to earn high profit, but similarly firms in the same industry will not do the same due to the fear of losing out profit. If a firm reduces the price to increase sales and profits.

Therefore, Oligopoly will lead to price rigidity in the market.

Share page on

NCERT Solutions Class 11 Economics

- Chapter 1 Introduction

- Chapter 2 Collection of Data

- Chapter 3 Organisation of Data

- Chapter 4 Presentation of Data

- Chapter 5 Measures Of Central Tendency

- Chapter 6 Correlation

- Chapter 7 Index Numbers

- Chapter 1 Introductions

- Chapter 2 Theory Of Consumer Behaviour

- Chapter 3 Production And Costs

- Chapter 4 The Theory Of The Firm Under Perfect Competition

- Chapter 5 Market Equilibrium

- Chapter 6 Non Competitive Markets

CBSE CLASS 11 NCERT SOLUTIONS

- NCERT Solutions Class 11 Physics

- NCERT Solutions Class 11 Chemistry

- NCERT Solutions Class 11 Biology

- NCERT Solutions Class 11 Maths

- NCERT Solutions Class 11 Accountancy

- NCERT Solutions Class 11 Business Studies

- NCERT Solutions Class 11 Economics

- NCERT Solutions Class 11 Geography

- NCERT Solutions Class 11 History

- NCERT Solutions Class 11 Political Science

- NCERT Solutions Class 11 English

CBSE CLASS 11 SYLLABUS

- CBSE Class 11 English Core Syllabus

- CBSE Class 11 Mathematics Syllabus

- CBSE Class 11 Physics Syllabus

- CBSE Class 11 Chemistry Syllabus

- CBSE Class 11 Biology Syllabus

- CBSE Class 11 Accountancy Syllabus

- CBSE Class 11 Business Studies Syllabus

- CBSE Class 11 Economics Syllabus

- CBSE Class 11 History Syllabus

- CBSE Class 11 Geography Syllabus

- CBSE Class 11 Sociology Syllabus

- CBSE Class 11 Political science Syllabus

- CBSE Class 11 Psychology Syllabus

- CBSE Class 11 Physical Education Syllabus

- CBSE Class 11 Applied Mathematics Syllabus

- CBSE Class 11 History of Indian Arts Syllabus

CBSE CLASS 11 Notes

- CBSE Class 11 Physics Notes

- CBSE Class 11 Chemistry Notes

- CBSE Class 11 Maths Notes

- CBSE Class 11 Biology Notes

- CBSE Class 11 Accountancy Notes

- CBSE Class 11 Business Studies Notes

- CBSE Class 11 Economics Notes

- CBSE Class 11 History Notes

- CBSE Class 11 Geography Notes

- CBSE Class 11 Political Science Notes

- CBSE Class 11 Entrepreneurship Notes

CBSE CLASS 11 BOOKS